Stable. Coin. Neither.

The name promises a digital dollar you can use anywhere, instantly, for anything. The reality is more complicated. Let's start from the beginning.

A person in Houston sends two hundred dollars to their family in Mexico City. Pesos leave one wallet. Dollars arrive in another. In between, invisible and instantaneous, a stablecoin sits on a blockchain for ninety seconds doing the work that used to take three days and cost a correspondent bank fee. This is the sandwich. Bread on either side is fiat currency. The filling is stablecoin.

Now ask yourself: what is this thing, really? Is it stable? Is it a coin? And if it works so well for remittances, why isn’t it being used for anything else?

Take the word apart. Stable suggests it holds its value. Coin suggests it is currency, something you exchange for goods. Put them together and you get a financial instrument that sounds reassuringly simple: a digital dollar, more or less, that you can move around on the internet.

Except it is not always stable. It is not always used as a coin. And depending on what is behind it, it can range from something close to a bank deposit to something closer to a bet that a piece of software will behave as designed.

What stablecoins actually have in common is this: they are crypto assets with a stabilizing mechanism. That mechanism is everything. It is what separates one type of stablecoin from another, what determines how safe they are, and what determines whether the word “stable” means anything at all.

Why not just hold dollars?

It is a fair question. If a stablecoin is pegged to the US dollar, denominated in dollars, designed to be worth one dollar — why not just hold dollars? Why introduce a new instrument at all?

The first answer is access. In Argentina, where the peso has lost the majority of its value over the past decade, holding dollars is both a rational decision and a logistically complicated one. Capital controls, banking restrictions, and a parallel exchange rate market have made dollar access uneven and costly. In South Africa, in Nigeria, in Lebanon, versions of the same story play out. People want exposure to a stable currency and the formal system does not always accommodate that want cleanly.

This is not a new impulse. Dollarization, formal and informal, has been a feature of developing economies for decades. What stablecoins added is programmability. A dollar-denominated stablecoin can be sent across a border in seconds, held in a self-custodied wallet, used in a transaction without a correspondent bank in the middle. The desire is old. The infrastructure is new.

The second answer is efficiency. Settlement on a blockchain is faster and cheaper than the traditional correspondent banking system. A wire transfer between two countries can take two to five days and pass through multiple intermediaries, each taking a fee. A stablecoin transaction settles in minutes, sometimes seconds, for a fraction of the cost. For remittances, for trade finance, for any transaction where settlement speed and cost matter, it is a meaningful structural advantage.

The desire to hold a stable currency is old. What stablecoins added is programmability.

What people are actually doing with them

So how are stablecoins being used today? Three ways, mostly.

The first is currency substitution. In countries with weak or volatile currencies, stablecoins have become a practical way for ordinary people and businesses to hold value in a more stable denomination. This is happening at scale in Latin America and parts of Sub-Saharan Africa. It is informal dollarization, running on blockchain rails.

The second is remittance settlement. The sandwich, as described above. The filling does the work. Nobody eats it as a meal.

The third is crypto market participation. For investors moving in and out of crypto assets, stablecoins act as a parking space. You close a position in bitcoin, convert to a stablecoin, wait for the next opportunity, convert back. The stablecoin sits at the on-ramp and the off-ramp. It is not the destination. It is the infrastructure you use to get there.

Notice what is not on this list: paying for your morning coffee. Buying groceries. Settling a restaurant bill. The US Congress, in passing the GENIUS Act in July 2025, defined stablecoins as “payment stablecoins” — instruments designed to be used as a means of payment or settlement. It is a reasonable ambition. It is not yet the reality. Stablecoins have found genuine utility in the economy, just not the one the name advertises.

The mechanism is everything

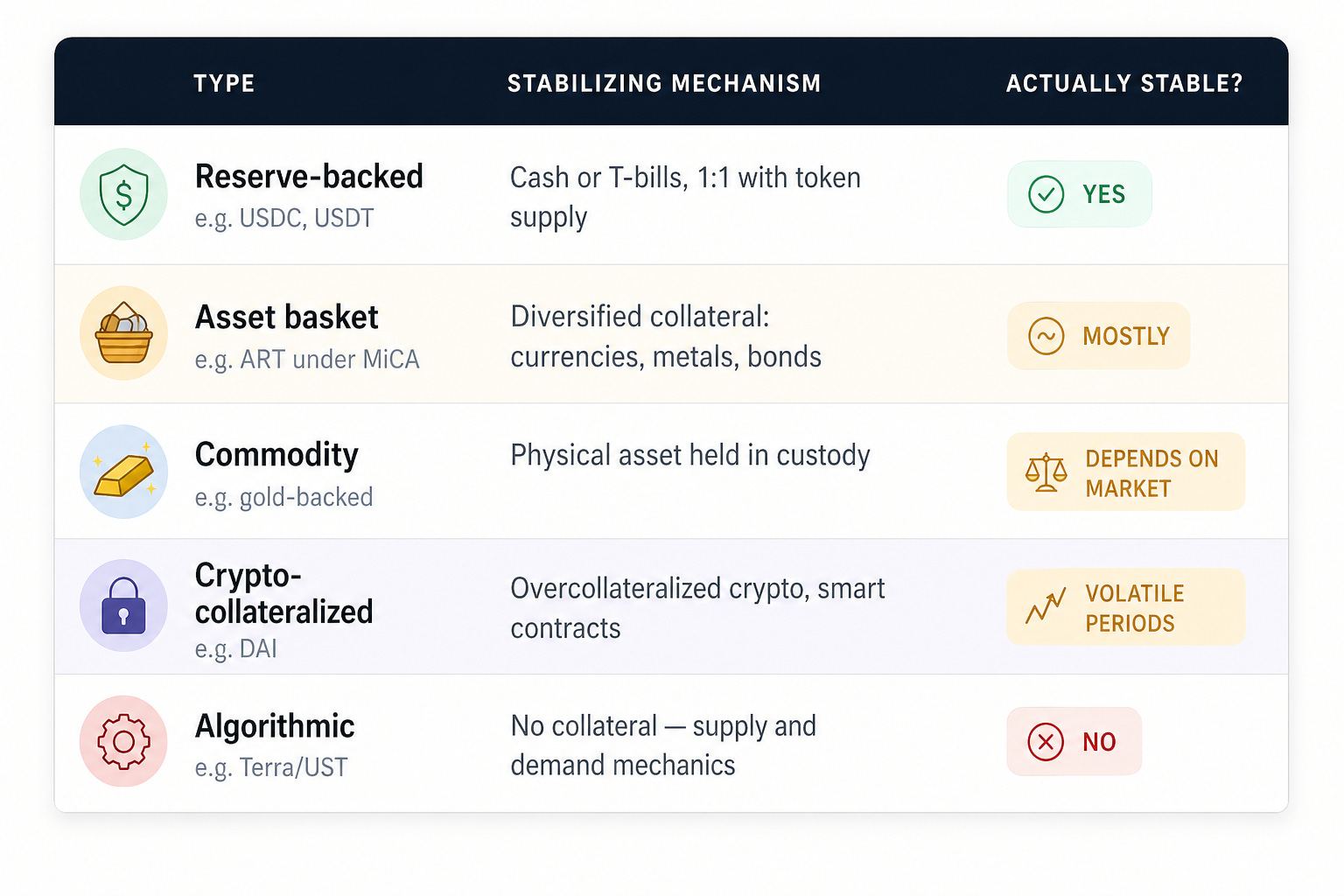

Back to the stabilizing mechanism, because this is where stablecoins diverge — and where the word “stable” starts to mean very different things.

The most straightforward type holds actual reserves. One token, one dollar, sitting in a bank account or a short-term Treasury bill. The peg is maintained because the money is literally there.

A second type holds a basket of assets — multiple currencies, metals, bonds — diversified to reduce the risk that any single asset’s movement breaks the peg. More complex, more opaque, but in theory more resilient.

A third type represents a physical commodity. Each token corresponds to a quantity of gold, or silver, or oil, held in custody somewhere. The peg is to the commodity’s market price, not to a currency.

A fourth type is backed by other crypto assets, overcollateralized through smart contracts to absorb price volatility. No bank. No vault. The collateral is code-managed and on-chain. Its stability depends on markets that are anything but stable.

And then there is the fifth type. No collateral at all. An algorithm adjusts supply in response to demand, minting tokens when the price rises above the peg, burning them when it falls below. The stability is maintained entirely by market confidence and incentive mechanisms. When confidence holds, it works. When it breaks, there is nothing underneath to catch it.

In May 2022, the algorithmic stablecoin Terra/UST lost its dollar peg in seventy-two hours. Approximately forty billion dollars in market value evaporated. The mechanism had nothing to fall back on when confidence broke. It was the most dramatic demonstration in the short history of stablecoins of what the word “stable” does not guarantee.

Not all stablecoins are equal

The five types are not equally stable. Reserve-backed stablecoins — the ones holding actual cash and Treasury bills — hold their peg reliably. USDC has maintained its dollar peg through multiple crypto market crashes. On that narrow definition, the name holds.

But move down the list and the ground shifts. Asset-basket stablecoins depend on the composition of the basket holding steady. Crypto-collateralized stablecoins depend on markets that swing violently. Algorithmic stablecoins, as Terra/UST proved, depend on nothing more solid than confidence. The same name, stablecoin, covers instruments with fundamentally different risk profiles. That matters — not just philosophically, but practically, for anyone holding one.

Stable in value. Fragmented in access.

So take the best case: a reserve-backed stablecoin, fully collateralized, reliably pegged. Is it stable? In value, yes. But stability is not just about the peg. It is also about accessibility. And that is where even the best stablecoins have a second problem.

USDC on Ethereum and USDC on Solana are not the same thing sitting in two places. They are the same asset on two different networks, and moving between them requires bridges — software protocols that lock tokens on one chain and mint equivalent tokens on another. Bridges carry their own fees, delays, and failure risks. Several have been exploited for hundreds of millions of dollars.

Instead of one large lake, you have many smaller ponds. Total water is the same — but you can’t access it all at once.

Different chains also have different liquidity depths. A stablecoin that trades freely on Ethereum may be thin on a smaller network, meaning large transactions move the price or cannot be executed at scale. So holding a stablecoin is not the same as holding dollars. Even if it is stable in value, it remains fragmented in access. The name promises both. The infrastructure delivers one.

Stable. Coin. Neither. Not yet.